To the average person, the hype around blockchain makes no sense. This series I will attempt to explain what the hype is about and what impacts it will have for you and your business and job as well as your life as a consumer.

This will end up being a multi-part series. I have been working on parts of this for a good chunk of 2018, working out explanations that I think are clear, testing them out on whoever I can that doesn’t work on blockchain technology. Making notes about what seems to connect, and tweaking what doesn’t.

Have you heard about Bitcoin?

So to kick off this series, I will start where most people have heard of through the news, and work from there. If you are like most people about a year ago in late 2017 you started hearing about Bitcoin and how it was worth a ton of money and growing at epic rates. you could put $10,000 into bitcoin and have 20,000 tomorrow. or 40,000 in a week.

No one could quite say why, but there was a generic belief in a few things, and there were two camps, one that jumped on the hype train believed something like this:

- It was the future of money, and

- If you got in now you could get a giant slice of that future and

- If you didn’t get in now, you might condemn all future generations in your family to poverty for missing out at this one window in time.

That there was a large group that held the opposite opinion was also true, some people believed something that was close to this

- As a replacement for gold, it imaginary money with no inherent value.

- As a replacement for PayPal or Venmo, it had little utility, wasn’t user-friendly, and was expensive and slow with scaling problems.

- As an investment, it was a tulip bulb level bubble/craze

Turns out, they are both right.

Greatest Hits tour from the 1900-1920s.

The run-up in prices was driven by some suspicious activity in the USDT market, that enabled folks to prop up an artificial price. This, as it turns out, is nearly identical to some of the stuff that happened in the Panic of 1907 on the NYSE (History of the US in Five Crashes) Limited transaction volume, driven in the BTC case by the HODL culture meant that a small group could “paint the tape” in “wash transactions” and create movement in the direction they wanted. In BTC trading circles coordinated groups that moved the market in preplanned ways were known as “whales“.

As it turns out all of these techniques featured prominently in the Panic of 1907 and the Black Tuesday crash of 1929 that marked the end of the roaring 20’s and kicked off the Great Depression.

But also, Blockchain is the future.

The core innovation that enables bitcoin to function is the “Blockchain”. And add to that the ability to write smart contracts and exchange digital title and tokens, you start to have the first glimpses of what the economic backbone of the world will be built on in 10-20 years.

In my opinion, the blockchain revolution will be easily 10 to 100 times bigger impact than the dotcom revolution of the late 90’s.

Where does Blockchain fit into the future?

This is how I tend to think about blockchain and how it ties to a business-oriented future of the internet and business.

First: Blockchain tracks exchanges between people: blockchain the way I think about it, it a public third ledger that lets any person or organization exchange something. What does it track? Blockchain by itself doesn’t specify anything. It is just a way to make a stream of data hard to impossible to alter once it has been created. What it tracks has to be determined. And the first really interesting use case was to track currency. And that leads up directly to the “killer app” for blockchain: Bitcoin.

**Second: Bitcoin is only one implementation, one that streams cash:**Bitcoin was the original proof of concept for blockchain. The question it attempts to prove an answer to is “Can we keep track of who has bitcoins, and record all the transactions between everyone on the network in one secure ledger?” The answer overwhelmingly has been “yes”. Bitcoin essentially proves the ability to point to point stream purely digital cash, without any middle-men or intermediaries.

It is a staggering proof-of-concept. But Bitcoin and streaming currency is not the only question that Blockchain answers.

Third: Blockchain can also track things that are unique, like the title to your house. Can we stream and track things that are discrete? There are a ton of items like that, where there is one and only one copy, and you cannot divide it. The title to your car or your house are two that everyone is familiar with. But there are other titles/digital items you may want to track. Like rights to a stream of an album of a video. Rights to a photo. And you can imagine all sorts of rules around those rights. But for now let’s assume that you want to transfer ownership of a discrete item. That is where something like a “Token” on Ethereum comes into play. The first big proof of concept here was CryptoKitties. That made use of beanie baby like collectibles that were stored on the Ethereum blockchain and could be traded and collected like you would baseball cards.

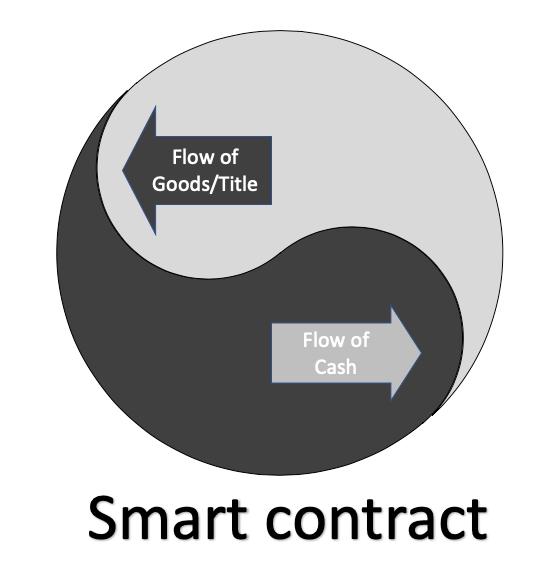

Fourth: If you can stream cash and title to goods, you have the basics of a new purely digital economy. While not particularly useful they were critical for one reason. Because you could trade a digital title for something, and exchange it for currency, in this case, Ethereum instead of Bitcoin you know have the first contract that starts to have all of the features of a real legal contract. Below is how I model that in my mind.

To have a valid contract you have to have one side sending cash, and the other side sending good back across. If you have ever dealt with any sort of marketplace you know that there is a bit of a disconnect between I send you money and you let me download something, or you send me something. If you order something from China or Ebay you will want some sort of escrow protection, where you put your money in, and until the goods are confirmed delivered your money doesn’t go to the seller. The smart contract here handles all that escrow functionality. one side places the digital title (token) in and agrees to the term. And the other side puts in the digital cash. Once the terms are met, the contract routes the items to the other party.

And here is the big thing. It is automatic and settles essentially instantly. Note there was not a bank in the mix here. There was not a marketplace. There was not a PayPal. this was essentially a self-organizing and executing transaction.

Fifth: For businesses, the impact will be even larger. Think about all the things that have to happen for a business to set up a contract with a partner in their supply chain and order some goods and make payment on those goods. It is a 30-60 day process probably in the best scenario. And it is littered with paper transfers and manual duplicate entry in your financial system and in theirs too.

A simple example might be something like this:

A ton of traffic back and forth,

- no direct linkage between your AP and their AR.

- no direct linkage between your inventory and theirs.

- Reconciliation between the two is impossible.

Think about how many times you have a conversation about “have you paid this invoice?” and you answer “we sent that” or “Why is this on this invoice, we already got billed for that item” or “you didn’t send that”

With a fully connected partner relationship, linked with a third ledger you will be able to have full transparency and visibility into the status of each transaction like that.

You will also be able to reduce a huge chunk of manual AP/AR/Inventory management.

And if you are auditing your business, think how much easier it will be to audit and attest to your financials. If your balance sheet shows inventory, you can quickly (in a matter of seconds) trace all of the transactions that support that inventory and which supplier attests to the fact that they sent the items. Similar story for your AR balance, is this a real invoice that someone else accepted and has agreed to pay? easy to prove and link. And many of the fraudulent invoices or bookkeeping manipulations are either not possible, or are trivial to detect. And the audit and attest program from your auditor should be a simple matter of giving them read access and allowing them to run some queries.

For businesses, it will be transformational.

Sixth: This will enable entirely new businesses that will operate exponentially faster. Once you have a structure of the smart contract. The ability to send tokens representing ownership. And the ability to stream cash for those assets. Once those parts are in place you immediately saw an explosion of “Initial Coin Offerings” or ICOs. Similar to an IPO, they allowed you to buy ownership into a company that had its ownership not in stock certificates but in ownership tokens or coins.

Here is an infographic tracking ICO growth. They went from essentially zero to $6.3B per quarter in less than 12 months. Astounding. And while that has been fraught with fraud, the glimpse of what is possible that they provide is staggering.

Businesses that can be formed as easily as a Kickstarter campaign.

Mergers and acquisitions that can happen with the transfer of digital assets around the world in minutes.

If you are a creator of digital content, you can take your viral video to the world and monetize it at the same time it goes viral.

Frictionless wealth transfer and content movement. It will be huge. Especially if your primary output at work can be loaded onto a thumbdrive. Digital content creators will be able to form new types of organizations that were never possible before.

Summary

Bitcoin may or may not be the ultimate way to stream cash in the future, but the underlying mechanisms that are built with blockchain will underpin the truly connected economy of the very near future. And you should start thinking about when you will jump in and how.